HRA Option-I would have been Beneficial than Existing Rates – Allowance Committee Report

Allowance Committee had recommended 3 options for HRA in its Report. If Option-I was picked for implementation from these three Options, it would have been beneficial than existing Rates.

House Rent Allowance (HRA) (Para 8.7.3-16)

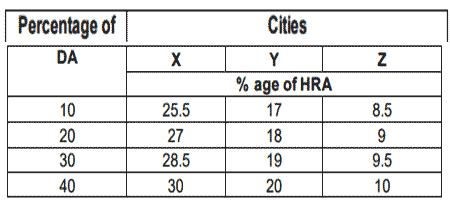

Existing Provisions: HRA is paid @30, 20 and 10 percent for X class (50 Lakh & above), Y class (5 to 50 lakh) and Z class (below 5 lakh) cities respectively.

At present, in the case of those drawing either NPA or MSP or both, HRA is being paid as a percentage of BP+NPA or BP+MSP or BP+NPA+MSP respectively.

Recommendations of 7th CPC: It has been retained and rationalized. After applying a multiplication factor of 0.8, the rates have been revised downwards to 24 percent, 16 percent and 8 percent of the Basic Pay for X, Y and Z class cities, respectively.

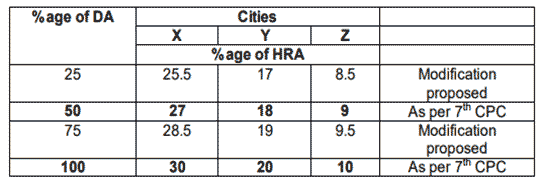

The rate of HRA will be revised to 27 percent, 18 percent and 9 percent when DA crosses 50 percent, and further revised to 30 percent, 20 percent and 10 percent when DA crosses 100 percent. Add-ons like NPA, MSP, etc. should not be included while working out HRA.

Demands:

I. National Council (Staff Side), JCM: HRA may be retained @30%, 20% and 10% for X, Y and Z cities respectively as the Commission has taken unreliable statistics to determine HRA, which has been reduced by a multiplication factor of 0.8 to 24%, 16% and 8% for X, Y and Z cities respectively.

II. CAG, Civil Aviation, M/o Health & FW, M/o HRD – D/o of Higher Education, MEA, Coal, DAE, DRDO, Dep. Of Space, CVC: Retain the allowance at the existing rates.

III. M/o of Law & Justice- D/o Justice: Cities having population of more than 1 crore may be granted HRA @ 30%.

Analysis and Recommendations of the Committee: The Committee has the following observations on the recommendations of the 7th CPC on HRA:

(I) HRA rates have been revised downwards by applying the multiplication factor of 0.8 applied by the 7th CPC on all percentage- based allowances. This was done to neutralise the significant increase in the Basic Pay. All fixed allowances have only been given an inflation indexed increase by the 7th CPC. While the 7th CPC has not explicitly stated how the multiplication factor of 0.8 has been arrived at anywhere in the Report, it may be seen that factoring in the expected Dearness Allowance of 125% on 01.01. 2016 would have yielded a multiplication factor of 0.875 which may have been rounded off to 0.8.

(II) On the 7th CPC recommendation that the rate of HRA will be revised to 27%, 18% and 9% when DA crosses 50 percent and further revised to 30%, 20% & 10% when DA crosses 100%, the Committee is of the view that given the inflation rates since January 2016 and the RBI policy on inflation, the DA rates might not go beyond 50% in the next 10 years.

(III) While the rents for residential accommodation have not gone up significantly in the recent past and might also have fallen in some areas, the HRA at the rates recommended by the 7th CPC at the lower levels might not continue to be adequate as per the prevailing market rent.

In view of these observations, the Committee has deliberated upon the following three options which separately, or in combination, can be suggested by way of modifications to the 7th CPC recommendations:

Option (i): Having regard to submissions made before it stating that towards the later part of the ten year period, HRA compensation falls considerably short of requirement, the 7th CPC has recommended that the rate of HRA will be revised to 27 percent, 18 percent and 9 percent when DA crosses 50 percent, and further revised to 30 percent, 20 percent and 10 percent when DA crosses 100 percent. However, considering the present inflation rate, the rate of increase of the Dearness Allowance and future inflation projections, it appears unlikely that DA rates will reach 100 % in the ten year period. Taking this into consideration, the Committee considered that the timing of the upward revisions in HRA rates proposed by the 7th CPC may be advanced as under:

This would have no immediate financial implication and the 1st revision, as per the current trend of increase in DA, is expected to occur in July, 2018. Accordingly, additional annual financial implication in July, 2018 will be approximately ₹1850 crore. The additional financial implication in the second, third and fourth revision will also be approximately ₹1850 crore per annum.

Option (ii): Instead of advancing the full restoration of HRA rates, the Committee considered splitting the revisions proposed by 7th CPC as under:

The financial implication would be similar as in Option (i) except that the timing of the revision would undergo a change.

Option (iii): It has been pointed out that at the recommended rates, HRA at the minimum level might not be sufficient. The minimum HRA calculated at the entry level of Level for X, Y and Z category cities at the rates recommended by the 7th CPC will be ₹4320, ₹2880 and ₹1440 respectively. The Committee considered recommending that the HRA at the rates recommended by the 7th CPC may be subject to a floor which may be fixed at ₹5400, ₹3600 and ₹1800 per month, calculated at 30%, 20% and 10% of the minimum pay for X, Y and Z category cities respectively. This will benefit employees in Levels 1, 2 and 3.

The additional financial implication is estimated to be ₹ 385.00 crore and around 7.70 lakh employees shall be benefited. After a detailed consideration of the above options, the Committee recommended that either only option (iii) or option (iii) in combination with option (ii) be accepted. A final decision in this regard may be taken by E-CoS.